Mankato Chapter 13 Bankruptcy Attorney

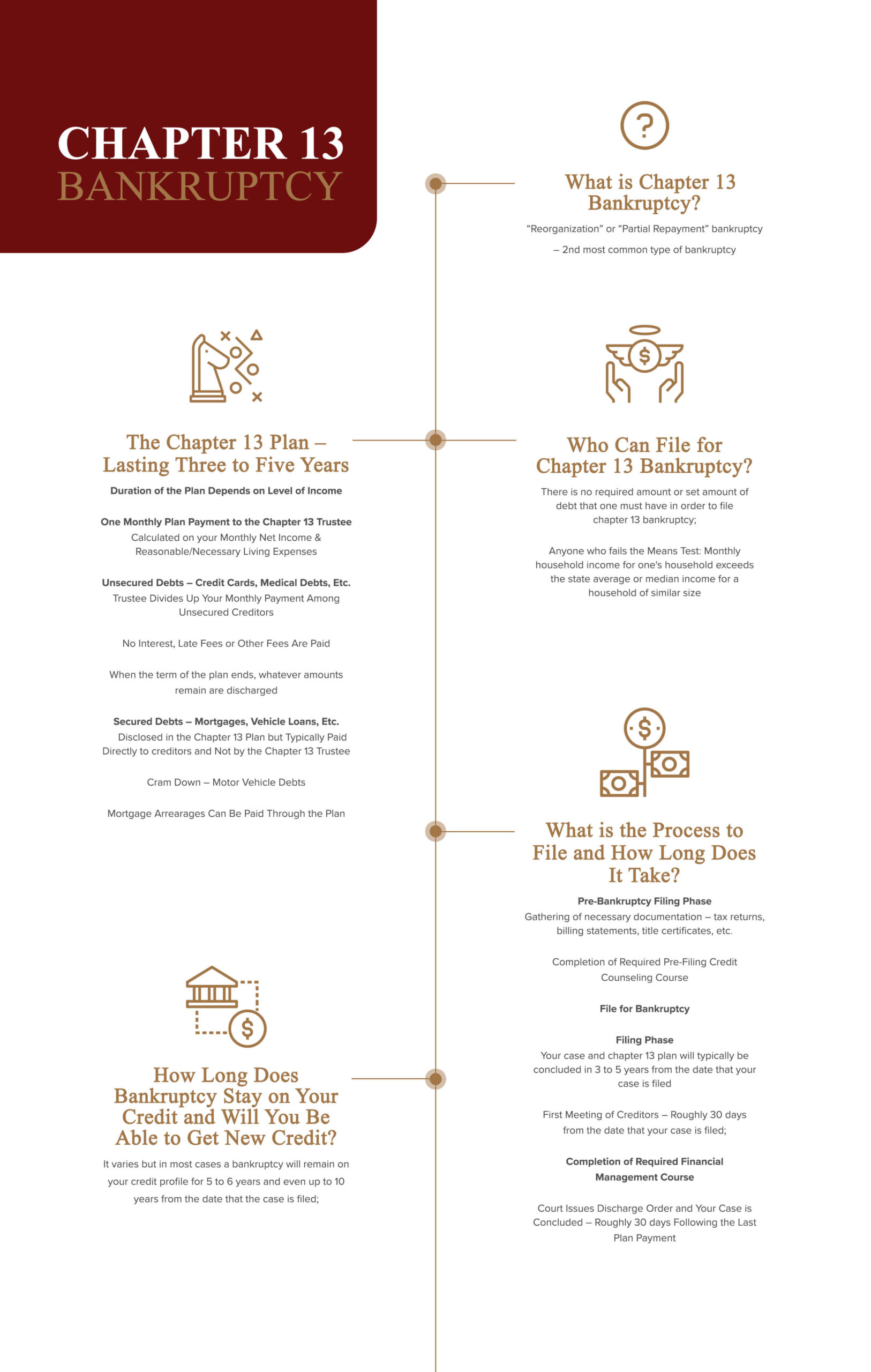

This type of bankruptcy is sometimes referred to as “wage-earner bankruptcy” or “debt repayment bankruptcy” or “debt reorganization bankruptcy.” In chapter 13, the bankruptcy court is presented with a plan for the repayment of a portion of your debts owed over a period of time, generally 3 to 5 years. In chapter 13, only a percentage of the debt is paid and not the entire amount. In a chapter 13 bankruptcy plan, you make a monthly payment to a chapter 13 trustee. The monthly payment made is determined by you and our office. Essentially, each month for 3 to 5 years, the bankruptcy trustee will split up your monthly payments among your creditors. In the meantime, the creditors cannot garnish your wages or repossess your property. This type of bankruptcy normally allows more time for creditors to

be repaid than would be available otherwise. Creditors cannot demand that a certain amount be paid and must accept whatever monthly payment your chapter 13 bankruptcy plan provides. No interest is paid; there are no late fees nor are there any other bogus charges to fret about. All payments are applied to the principal of your debts.

In order to file chapter 13, you must have consistent, regular, and stable income either from a job, social security or other viable resource; and there are limits to the amounts of debts you can have. For instance, there cannot be more than $360,475.00 worth of unsecured debts (credit card debts, medical debts, personal loans, and other debts for which no collateral has been pledged) and no more than $1,081,400.00 worth of secured debts (mortgage debts, vehicle loans, and other debts for which collateral has been pledged in order to guarantee payment).

click to learn more about

CHAPTER 13 BANKRUPTCY

There are many benefits in filing a chapter 13 bankruptcy, including, but not limited to, the following:

- You can prevent a mortgage foreclosure and pay back a mortgage delinquency over 3 to 5 years instead of in one lump sum;

- You can strip off wholly unsecured second and third mortgages off of your home;

- You can pay back tax debts at no interest over 3 to 5 years;

- You can pay back a child support delinquency at no interest and at no risk of being garnished over 3 to 5 years;

- Certain older tax debts that were timely filed are completely discharged;

- Your bankruptcy plan is court supervised, so you have more resources to monitor the activities of your mortgage creditor or vehicle creditor to ensure that they are following the rules and are not charging you bogus fees;

- You can file a chapter 13 bankruptcy even though you may have filed a chapter 7 bankruptcy within the last 8 years;

- You can cram down a vehicle loan debt to the present value of the vehicle and pay only the present value of the vehicle in your plan and receive the title certificate for the vehicle when your bankruptcy is concluded;

- You can cram down interest rates on vehicle loans;

- You can keep non-exempt property that you would otherwise lose in a chapter 7 bankruptcy;

- More debts are discharged in chapter 13 than in a chapter 7 such as debts incurred through divorce and through willful and malicious injury to another person and fines and penalties to governmental units ;

- You can object to and disallow claims for payment submitted by your creditors;

- In certain circumstances, you can repay a student loan debt on more generous terms than those demanded by the student loan creditor;

- You have the ability to voluntarily dismiss your case at any time as long as the dismissal is not for fraudulent purposes and you can convert your case down to a chapter 7 case if your circumstances change;

- You could conceivably be in chapter 13 bankruptcy forever since the bar between filing chapter 13 bankruptcies is only 2 years. In other words, once you get out of your 3 or 5 year chapter 13 bankruptcy you could file another one without having to wait at all.

How Does Chapter 13 Bankruptcy Work?

In chapter 13 bankruptcy, you and our office would determine the amount of your monthly plan payment by first going through your monthly income and monthly expenses. In other words, we would set your monthly net income against your monthly necessary living expenses and see if there would be any money left over. When we determine your monthly expenses, we do not include debt repayments for such things as credit card debts or medical debts or debts owed to friends and relatives or past due amounts on utility charges or overdraft protection charges and the like because those debts would be included for payment through your bankruptcy plan. Rather, we count expenses such as ongoing mortgage or rent payments, ongoing vehicle loan payments, insurance for your vehicles, food, charitable contributions, recreational expenses, gasoline for your vehicles, and other expenses that are reasonable and necessary for you to live and maintain a household on a day-to-day basis. After determining your monthly expenses, any surplus income would represent your plan payment. For instance, if your monthly net income were $3,000.00 and your monthly reasonable and necessary living expenses were $2,800.00, your monthly plan payment to the chapter 13 trustee would be $200.00.

Your chapter 13 plan is a very powerful tool because, once it is approved by the bankruptcy court, it operates as a binding contract that modifies the claims of your creditors. Your creditors are, in fact, bound by its terms and they are obligated to comply with it. During your chapter 13 case, your plan can be modified if your circumstances change. For instance, if your income were to decrease your plan could be modified to allow you to make lower payments.

In chapter 13 bankruptcy, the procedures are basically the same as they are in a chapter 7 bankruptcy case. Once your case is filed, the automatic stay goes into effect prohibiting creditors from taking or continuing to take any collection action against you such as harassing telephone calls, repossessions, garnishment of wages/bank accounts, and foreclosures. Like in a chapter 7 bankruptcy, you will have a bankruptcy hearing with the trustee about 30 to 45 days after your case is filed and one of our attorneys will appear with you. As with a chapter 7 bankruptcy proceeding, the chapter 13 hearing usually lasts only 5 to 10 minutes and you are sworn under oath and are asked questions about your bankruptcy petition and related schedules to ensure that they are accurate.

In chapter 13, you start making your plan payments to the trustee 30 days after your case is filed according to your chapter 13 plan. About 15 to 20 days after your hearing with the chapter 13 trustee, there will be a second hearing where your bankruptcy plan is presented to the bankruptcy court for approval. You do not need to attend this hearing unless you hear otherwise from one of our attorneys because your bankruptcy plan will usually be approved by the bankruptcy court by default. Your payments will continue until the completion of your plan in 3 to 5 years. Whether your plan must go 3 or 5 years depends on the level of your projected household income. If your projected household income is higher than the state average income for a household of your size, your plan must go for 5 years. If your projected household income is less than the state average income for a household of your size, you can choose whether to have your plan go either 3 or 5 years. Once your plan is completed, the bankruptcy court will issue you a discharge order and whatever portions of your debts that were not paid through your bankruptcy plan will be discharged.

Bankruptcy law requires that you complete two financial courses, one before your case can be filed and one after your case has been filed. Both of these courses can be done either over the telephone or over the internet and you will be issued certificates of completion for each course which must be filed with the bankruptcy court. The first course you will take is a pre-bankruptcy course called credit counseling which is designed to help you review and evaluate your financial situation. The second course, called debtor education, is taken after your case is filed and you must complete it in order to receive your chapter 13 discharge. This course is designed to help you better prepare for your financial future, and you will receive tips on things such as how to budget better and how to distinguish “good debts” from “bad debts.”

Find Relief With a Professional Chapter 13 Bankruptcy Attorney Today

Chapter 13 bankruptcy can be the first step to recovering from debt. An experienced bankruptcy attorney can help you navigate these complex legal waters and advocate for your best interests. Contact Behm Law Group, Ltd. today to regain control over your life and your future.